Below is an post from curbed boston showing properties in different Cape Cod neighborhoods with asking prices of $250K. Curbed Boston left out our little fishing village of Provincetown. I just had to add it to the list… and with two properties…for an interesting Cape-wide comparison. Again, I apologize for grammar and spelling in the property descriptions. The copy was lifted directly from the blog and from MLS.

These few properties are but a small sampling of those available Cape wide in this price range. Buyers are constantly surprised when we are able to show them delightful and very livable properties in this price range. In Provincetown alone there are 42 properties with asking prices of $300K or less.

This is a delightfully light and airy 1 bed/1 bath condo of 454 square feet. Renovated and Charming East End One Bedroom Condominium. Sneak peeks of the water from every window. Beach access across the street. New hardwood floors in the living room. New carpet in the bedroom. Small 4 unit association. Pets for owners. Common laundry room with some storage for owners. Shared back yard. Weekly rentals permitted. This unit is priced to sell quickly. Condo fee includes hot water, building insurance, water and sewer, common area maintenance..

608 square foot, 2 bed/1 bath condo with a total cosmetic interior renovation including new

floors, kitchen and bathroom cabinets, counters, lighting and paint. Located in the heart of Provincetown, downtown between the two wharfs. This is a top floor unit above commercial spaces below. It is well designed to provide two good size bedrooms, 3 huge closets, and bath with tub. Redesigned galley kitchen with bar counter opens to bright living room. New window treatments and AC units for each room are included in the offering. Pets and weekly rentals are allowed.

In Wellfleet, at 420 Chequessett Neck Road, a 352 sq. ft. cottage built in 1945. Located in Chequessett Village with a stoner-friendly address, the property has been renovated “to the studs.” The two bedroom, one bath is fully insulated and includes two new skylights, energy efficient heat, wood flooring, Corian counters in the kitchen and bath, and a rear deck. The condo first hit the market in March with an asking price of $275,000. Three pricechops have brought the listing down to $250,000.

Over in Sandwich, at 24 Tabor Roadwe find a 1,001 sq. ft. two bedroom, two bath ranch. Built in 1975, the updated Forestdale neighborhood property features hardwood floors, an eat-in-kitchen with custom cherry cabinets and new appliances, formal living and dining rooms, radiant heat, air conditioning and a new bathroom. There’s also a lower level family room and home office. Outside, the .24 acre property includes a deck, shed and “great landscaping.”

In Harwich, at 228 Chatham Road, we find an opportunity for some “This Old House” action. The repetitive brokerbabble doesn’t have much to say other than, “RESTORATION OPPORTUNITY. CIRCA 1750 CAPE IS ALL ORIGINAL READY FOR RESTORATION.” Apparently, the photos speak for themselves. The 1,117 sq. ft. antique includes three bedrooms, one bath in eight rooms. In addition, the .94 acre property also includes some sort of out-building (Shed? Garage? Barn?)

Over in East Falmouth, at 804 Old Barnstable Road, we find a three bedroom, two bath with a “surprise inside!” According to the brokerbabble, “A sweeping boudoir Master Bedroom on the 2nd level removes you from a strenuous, hard days work and recaptures what life’s all about,” placing you into a hodgepodge of bathroom trends, from 1980s glass blocks to a vessel sink straight out of the early aughts. There are also two first floor bedrooms, along with a kitchen that “sweeps and opens” to the living room in the 1,110 sq. ft. Cape. The property last sold in March 2008 for $235,900.

Get a Glimpse Inside the South End’s Coolest Homes on the South End House Tour

This year’s South End House Tour will take place on Saturday, Oct. 20.

by Sara Jacobi…South End Patch

It’s a little bit like the History Channel meets HGTV. Right in your backyard.

Get a peek into several of the South End’s historically notable or highly designed homes on the 44th annual South End House Tour, put on by the South End Historical Society.

The tour, to be held on Saturday, Oct. 20 from 10 a.m. to 5 p.m., is a self-guided walk through six amazing South End homes starting at the Southwest Corridor and ending mid-way down Shawmut Avenue. Since the tour is at-your-own-pace and snakes around on a more than 1 mile path, the full tour can take anywhere from two to four hours. It starts at the Boston Center for the Arts.

South End Historical Society Executive Director Hope Shannon said the idea for the house tour began more than four decades ago as a way to showcase the creativity and history of the neighborhood.

“People were buying a lot of run down or abandoned buildings in the South End and restoring them,” she said. “The neighborhood was much different back then.”

Today, the tour seeks to showcase all sorts of notable homes, from the historical, to the “green,” to the homes with unique architecture or high design.

Special to the 2012 tour is a combination deal with the Ellis Memorial Antique Show, which will be held at the Cyclorama on the same day. A ticket to the house tour comes with a complimentary admission to the antiques show. This year’s tour will also feature a stop inside the New Hope Baptist Church, which will soon be turned into condo apartments.

Shannon said that besides serving as a significant fundraiser for the historical society, the house tour’s main goals are to continue bringing people into the South End and to showcase the neighborhood’s history and charm.

“The neighborhood has changed so much, and the homes have so much history,” she said. “We want to remind people of the long history and bring awareness for continued preservation. We want visitors to leave with positive memories of the people they meet and the businesses they patronize, and recognize the South End is an important place historically.”

Tickets are on sale now through Oct. 19 for $25, and can be purchased online at the Historical Society’s website or through several different realtors in the neighborhood. Tickets will also be on sale on the day-of for $30 each. A $50 ticket includes admission to a private party at an additional house.

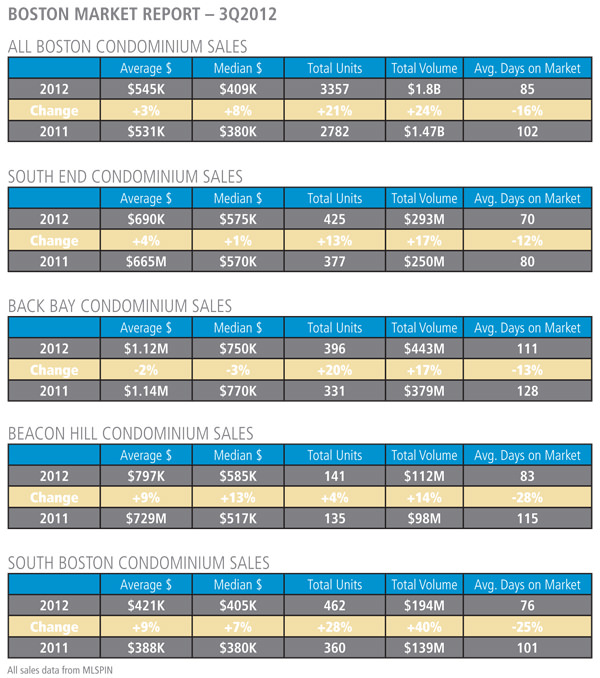

The Big Number is 21%. That’s the increase in condo sales year over year at the end of the 3rd quarter, September 30. Combined, all Boston neighborhoods saw a 21% increase in the number of condo sales year to date, a 3% increase in the average price of a condominium sold to $545K, and an 8% increase in the median sales price to $409K. This real estate market is healthy except for the continuing decrease in inventory levels. Inventory levels of available condo’s for sale have fallen 41% to 919 properties for sale versus 1,567 at this time last year.

The Back Bay, saw a 20% increase in sales year to date, but the average price of a condo sold dropped by 2% to $1.120M. The inventory level of condos for sale dropped 53% to 95 condos for sale vs 204 last year.

The South End saw a 13% increase in the number of condo sales to 425 condos sold year to date compared to 377 last year. The average price of a condo sold increased 4% to $690K compared with $665K last year. The inventory of condos for sale decreased 52% from 173 last year to 83 today. This will continue to be a factor in market performance going forward.

South Boston saw a 28% increase in the number of condo sales year to date compared with 360 last year. The average sales price of a condo increased by 9% to $421K compared with $388K last year. South Boston has the largest drop in inventory of all downtown n’hoods down 60% from 196 properties for sale last year to 78 available for sale today.

Inventory remains the problem, but as I have said repeatedly this market is so resilient and so desirable that declining inventory levels have not negatively effected the steady increase in sales and prices. Go figure!

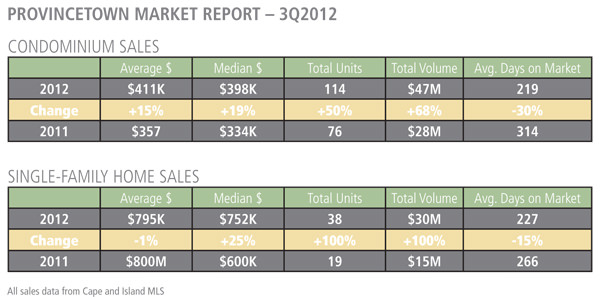

What a summer we have had in Provincetown… the great energy that we began to see in the second quarter continued into Q3. Ongoing economic optimism and low interest rates continue to attract buyers. We are seeing a wonderful phenomenon here where buyers who have been on the sidelines have decided to jump into the market. With such a wide variety of properties for sale – both in price and character – buyers have much to choose from.

Year-to-date condominium sales through September 30 totaled 115 properties – a full 50% more than last year’s 76 sales. The average selling price for a condo was $411K – a 15% increase from last years $357K. The median selling price was $398K – up 19% from $334K last year. And condos sold at an average 95% of asking price.

Total sales volume in the condominium category was $47M year-to-date compared with $28M last year – a solid 68% increase. Days-on-market, an important indicator of market strength, decreased 30% to an average of 219 total days-on-market from last years 314. There are 134 condos on the market today with an average asking price of $481K with an average of 804 square feet and $598 per square foot.

Sales of single-family homes increased even more dramatically to 38 units – a 100% increase from last years 19 single-family home sales. The average selling price was $795K – a 1% decrease from $800K last year. Total sales volume on this category was $30M compared with $15M last year – a 100% increase. Average total days-on-market decreased 15% to 227 vs. 266 last year. There are 72 single-family properties on the market today with an average price of $1.388M and 2,295 square feet at $605 per square foot.

Fall is one of the busiest selling season’s here, so we look forward to more good news in our year-end reporting. But, that is a full three months away. A lot can happen in that time!

If you are visiting for Halloween, Holly Folly, or New Years, stop in to say hello.

A great Boston Globe article below. The Herring Cove Bathhouse’s last hurrah!

Events to honor Cape Cod bathhouse

By Cate McQuaid

| GLOBE CORRESPONDENT SEPTEMBER 27, 2012

JULIA CUMES

Artist Jay Critchley places a found flag on bathhouse benches outside the Herring Cove Beach bathhouse in Provincetown as part of his upcoming art installation/show.

PROVINCETOWN — The bathhouse at Herring Cove Beach is on its last legs. The nearly 60-year-old modernist structure dominates this little slip of the National Seashore at the tip of Cape Cod, but the floors are cracking, and the second floor was condemned years ago. Demolition will begin in October.

But the bathhouse is going out with a bang. Artist and impresario Jay Critchley has spearheaded “Ten Days That Shook the World: The Centennial Decade,” featuring art installations, performances, panel discussions, video screenings, and more at the bathhouse and on the beach, Sept. 28-Oct. 7. Friday’s opening includes a campfire and marshmallow toasting on the beach, with music by Screem Along with Billy/Clap for Sue and Magic & the Reggae Stars.

“It’s a classic modernist structure, built as a fortress to protect us from nature, and now nature is encroaching,” Critchley said of the bathhouse. On a blustery, sunny day earlier this week, as electricians laid cable through sand and artists busily worked around the bathhouse, he was taking a break in the musty-smelling lifeguard lounge.

Critchley is known for running the Provincetown Swim for Life & Paddler Flotilla benefit, and for a variety of comic, politically incisive art projects. These include his massive multi-artist 2007 installation “The Beige Motel,” for which he completely encrusted a North Truro motel in sand and invited artists to create installations in the rooms. But even with Critchley’s experience organizing such events, “Ten Days That Shook the World” has been a marathon run at a sprinter’s pace.

Ten Days That Shook the World: The Centennial Decade

“The bathhouse was originally going to be torn down in 2014,” he said, and he had spoken to George Price, National Park Service superintendent for the Cape Cod National Seashore, about doing the project then. “But money came in early, and I got a call from George in July.” Critchley said. “It was a two-year planning project in two months.”

More than 30 events will touch on themes such as the environment, time and impermanence, and Provincetown’s inception as an art colony 100 years ago, between 1910 and 1920. “Ten Days That Shook the World” is held under the auspices of the Provincetown 10 Days of Art 2012 Festival and the Provincetown Community Compact. The event’s title refers to journalist and activist John Reed’s account by the same name of the Russian Revolution in 1917. Reed was also an early member of the Provincetown Playhouse, founded in 1915.

“That decade was the progressive era in American history,” said Critchley. “There was suffrage, birth control — Margaret Sanger was in Provincetown. There was the labor movement, muckrakers. Then World War I came, and the government started cracking down on activists.” He sees parallels today, he added.

History-themed events will include actor Tim Babcock’s performance “1912 or 2012? You Decide,” a couple of renditions of plays by Eugene O’Neill, a Provincetown Playhouse founder, and a panel discussion, “Provincetown’s Centennial Legacy: State of the Art Colony.”

While Critchley spoke about “Ten Days,” artists were at work on their installations. Vicky Tomayko and Maryalice Johnston had set up a work table covered with paint and stencils in the men’s changing room, and were painting female figures and fish in the shower stalls. Jennifer Hicks had filled the original electric utility room with sand, gauzy fabric, and sparkles, and intended to create a nest on the floor complete with giant eggs visitors might sit on.

“It’s about the tree swallows roosting around here right now,” Hicks said. “There are thousands of them, eating bayberries.” In addition to her installation, Hicks is scheduled to lead a free class in Butoh, an image-based Japanese dance tradition, on Sept. 29 followed by a performance on Sunday. “I’ve got everyone a hazmat suit, and people will be painting birds on their backs as they move,” Hicks said.

Outside, Paul Wirhun was covering the concession stand with designs and illustrations in tape. He planned to paint the walls, then remove the tape to reveal a seascape. Inside, photographer Marian Roth had boarded over the windows of the hot dog stand in order to turn it into a giant pinhole camera. According to Critchley, performance artist Heather Kapplow will take over another portion of that building Oct. 6, and invite visitors to make their own concessions.

Every evening, there will be a campfire on the beach, and the bathhouse will be lit.

Next summer, visitors to Herring Cove Beach will have new facilities. Several smaller shingled buildings, linked by boardwalks, will provide a more intimate experience compared with the bulwark of the old structure.

“This isn’t charming,” said Critchley. “This is monolithic. It’s out of character with the landscape and architecture of Cape Cod. But this is a monument. People wouldn’t build anything like this again. It’s an excess of material, an excess of space.”

He was standing on the concrete platform that separated the building from the beach, squinting at the few tiny windows along its beige walls. “There’s a determinism to this building, that it will last forever. It is a self-righteous and in a way arrogant building. And it has held its ground for 60 years,” he said.

The wind riffled his shirt. “But the times are a-changing,” he said, “and the climate is a-changing.”

We are thrilled to announce our new website at Beachfront Realty. Take a look by clicking anywhere on the image below. We have a terrific new search function that is easy and smooth. If you want to stay on top of what’s for sale go to register/login on the top right of the site! Properties for sale that fit your criteria will be emailed to you daily. Enjoy!

My good friend, excellent agent and blogger Briggs Johnson at Coldwell Banker Residential Brokerage hits it squarely on the mark with this post which illustrates the decrease in inventory year over year and its potential effect on the market. I have posted it in its entirety below. Visit his blog.

There are several indicators and indexes that people follow to determine market conditions. The indicator I am going to use that sparked this blog entry is going to called the “Caravan Indicator”. What many people don’t know is that behind the scenes here at Coldwell Banker (downtown), every few weeks, we hire a bus to drive us all around town to check out new listings in Back Bay, Beacon Hill, South End, South Boston and the Seaport District etc. Its a great way for us to view new inventory and for us to be knowledgeable of the market in all price points. Today, is caravan day and it was cancelled due to lack of inventory…..Wait, What?! I can understand there being a cancelled caravan in late fall or August when everyone is on vacation, but not now, not September, not in the second week of the second strongest time of year to get new inventory. Really?

I was ready to bounce around the city and view some properties, but, since that wasn’t happening, I did some research to see how limited inventory really is. I went on MLS and looked up current inventory, the amount of listings currently under agreement and the amount of listings that have been sold in the past 2 months. The numbers don’t lie and I found them pretty shocking. Since I really only focus on the downtown neighborhoods. I used the 4 neighborhoods i do a lot of business in . Here are the Stats:

Neighborhood # of Listings # Under Agreement # Sold in last 2 months

Back Bay 104 57 124

South End 78 57 110

Beacon Hill 59 14 41

Seaport District 16 7 23

Last Year (2011) # of Listings % Decrease from 2011

Back Bay 213 52%

South End 183 58%

Beacon Hill 82 28%

Seaport District 37 57%

The way I look at this information is that it is a great time to sell and list a property. There are a ton of buyers out there and they are in desperate need of decent inventory. On the flip side, If you are a buyer looking in these neighborhoods, be prepared to be frustrated and be ready to enter a multiple offer situation (if you are a serious buyer looking in a popular area). In the South End alone there have been 24 places go under agreement in the past 2 weeks. If you are a buyer looking in the South End under $450k. there are only 9 places on the market and only 3 of them are north of Washington Street. If you are a buyer looking in the 800-1 million range in the Back Bay, there are only 11 listings on the market. Six of those listings have been on the market for over 100 days, so quality is as compromised as quantity right now. If you are a Beacon Hill buyer looking from 600-900k there are only 3 listings on the market. 2 of those listings have been on the market for over 170 days. Brutal!!

I can understand that sellers are hesitant to list because there isn’t much to move into if they sell and want to stay in downtown Boston. But if you are a possible seller looking to move out of state or to the “burbs” this could be an ideal time to make the jump.

I know all downtown agents are saying “list your property now” but hopefully some of this data, makes you think about the scenario with a different tone. Have hope and don’t be afraid to enter the market, just be informed and realistic.

The $1M and above market in Provincetown has been relatively active this season. The above $1M price range is from $1M to a high of $4.75M. Of the 136 properties (single family, Multi-family and condos) that have sold YTD in 2012, 8 have sold above $1M, and they were all single family properties. These 8 property sales equals 5% of total unit sales year to date.

There are 218 properties (singles, multis, and condos) for sale in Provincetown of which 55 are priced above $1M, which represents 25% of the total.

5% of sales, 25% of the available properties for sale… it is crowded! For buyers in this price range there are plenty of properties to look at for price and amenity comparison. Currently there are 5 properties under contract with asking prices above $1M. I will profile these once they close.

Below are descriptions of the properties that have sold over $1M year to date. Once again a caveat. I took the descriptions straight from MLS, so errors in syntax and grammar are out of my hands.

67 Bayberry Ave SOLD $1.05M

67 Bayberry Ave, a contemporary home, impeccably maintained, this home is bright and airy, white washed in a soft colors, and is ideal for entertaining with an open plan along with 3 bedrooms. Enter through glass doors to a spacious living room with fireplace, a kitchen & separate dining room that comfortably seats 10. The living room has two sets of atrium doors leading to a covered deck and large terrace. The kitchen has custom cabinetry, and limestone counter tops. There is a guest room with deck on this level with full bath. Next level has an open den, and mb suite with separate bedroom and sitting room with fireplace, bath and deck. The 3rd bedroom is on this level with another bath. Up one more level is an intimate sun room with 3 decks.

510 Commercial St SOLD $1.05M

510 Commercial Street is a lovely single family home with water views. The 1st floor has a spacious living room with fireplace, generously sized dining room, recently renovated kitchen, laundry area and full bath. There is also an adjoining one bedroom, one bath apartment with exclusive outdoor space, perfect for guests. Upstairs there are two master bedrooms with ensuite baths, one of which has direct water views. A second guest room with water views and full bath complete this level. The home is well set back from Commercial St allowing for a spacious front yard and privately situated side yard with patio. Driveway parking for 3 cars in tandem.

3 Atlantic Ave SOLD $1.065M

3 Atlantic Ave. Very few people have enjoyed the pleasure of owning this West End historic home. One of Provincetown’s oldest homes, dating back to the 1700’s, this A+ quality recent restoration makes this pristine home an exceptionally rare opportunity. The original architectural details have been painstakingly preserved side-by-side with the highest quality contemporary fixtures, appliances, systems, windows, doors, and more. The value is further magnified by both the central location-steps from the beach-and the generous enclosed yard space for parking, entertaining and gardening. The current owners have taken extreme care to bring this three-quarter Cape style home into the 21st century with a great deal of love and attention.

19 Berry Lane SOLD $1.093

19 Berry Lane. Steps from the Beach and Views from Every Room! Here is Your Opportunity to Own a Custom Built Provincetown Home in the Quiet East End. From the Moment you enter the Foyer you will feel a sense of peace and serenity. The Living Room has Custom Stained Glass Windows from an old N.H. Church (easily removed, decorative only), hardwood floors and balcony access. The 2 Story Family Room offers a solid wall of windows, designed to maximize the expansive views,Brick fireplace with Bluestone Hearth and accent wall. Watch the Harbor lights from the Dining Room. Entertaining is a breeze in this Spacious, light filled Kitchen! Upstairs you’ll find the Owner’s Suite with Spa Quality Bathroom and the Guest Wing with 2 Bedrooms with views. Full Daylight BSMT also w/ views, 2 car garage.

9 W Vine St SOLD $1.2M

9 West Vine Street. Completely renovated 5 bedroom 4 bath home located in the heart of the West End. There is a spacious living room, dining area and kitchen on the first floor which opens to a blue stone patio and fenced in yard. The kitchen features a large center island, granite countertops, a farm sink & marble backsplash. There is a master bedroom suite with a private tiled bath and separate entrance, a second bedroom and tiled bath on the first floor. The second floor features a second living or family room with gas fireplace, in addition to an office, three more bedrooms. Stained pine & fir flooring in all living areas, Laundry room, ample closet space, an unfinished attic, outdoor shower, & 2 car parking.

525 Commercial St SOLD $1.25M

525 Commercial Street. Funky East End bay front home with multiple personalities. The original structure appears to be a marine related or mercantile structure dating from pre-1800 and is now known as the Not So Great Room with soaring 2 story ceiling and original folk art found object installation by Jackson Lambert. A 20th century addition is a large sunken living room with brick fireplace, wood floors and bay windows facing Commercial St and the bay. The most recent custodians of this gem added a contemporary solarium and deck on the bay and updated the kitchen and second floor bath a few years ago. Estate sale. Offers are subject to estate obtaining a license to sell from probate court. Town sewer outstanding betterment of only $2,295.41, to follow deed

107 Commercial St SOLD $1.6M

107 Commercial Street. There are only 15 single family waterfront homes in the west end – not since 2004 has one come to the market below $2M. Don’t miss this opportunity to purchase the perfect beach house in the perfect location that usually exists in dreams. This charming 3-BD, 2-BA waterfront home enjoys great privacy and spectacular views. 1st floor has an open floor plan, exposed beams, wood-burning stove and fireplace (not in working order), with sliders leading to front and side yards and large waterfront deck with steps to the beach. Also on this level are a full bath and laundry. The 2nd level has 2 waterfront bedrooms with sliders to a common deck with ladder to rooftop deck. There is also a 3rd BD and BA on this level. 3-car parking, Sewer Connection.

6 Winston Ave SOLD $1.8M

6 Winston Ave. Spectacular Waterfront Home with breathtaking views of Cape Cod Bay from almost every room. Talk about inspiration and beauty! There are 4 bedrooms in this magnificent home with the master on the second floor, gas fireplace, dazzling views of the water, a large elegant master bath, and a door leading to your private deck overlooking the water. Another bedroom shares those same views and deck, along with a full bathroom that separates the second and third bedrooms upstairs. First floor is full of light with a virtual wall of sliders that open to an expansive deck for your sunny enjoyment and relaxation. A large stunning kitchen with Granite counter tops, a first floor bedroom or office and a new artist studio with more gorgeous views of the water. Offered at $2,350,000.

This is an interesting blend of East End, West End, and downtown properties. My favorites are 3 Atlantic as it is in the near east end on Atlantic and Commercial and just smack in the middle of things on one of the most special streets in town. 107 Commercial is a favorite as it is one of those special properties right around the bend from the Coast Guard Station in the west end that is the epitome of casual downtown beachfront living… everyone who walks by it says…”I wish I owned that house.”

*Data is for single families, multi families and condos only sold from 1/1/12 to 8/31/12. There are some additional properties for sale in Provincetown like hotel/motels, and commercial properties which I do not generally include in my analysis of residential sales. All data from Cape Cod and Islands MLS.

I am thrilled to be here at Beachfront Realty in Provincetown – a great, truly local real estate company with broker owner Bob O’Malley and my associate Bill Farmer. We have had an exciting spring/summer season and are looking forward to experiencing the serious fall selling season.

I will post on all things real estate. Architecture and design, market trends and market drivers, the ever changing and always challenging movements in the Provincetown and Outer Cape, Boston and South Florida markets, markets that are related in many ways. This unique forum will enable us to talk about everything related to real estate.

My blog will feature regular postings from me and from a range of other professional contributors within the industry. It will also include occasional posts from knowledgeable guest contributors across other market areas. Ultimately, my blog will focus on timely and provocative real estate articles of interest and, I will look to all of you for new ideas and opinions that will keep the postings fresh, raise thought-provoking ideas and deliver entertaining stories that will challenge all of us to keep the dynamic real estate conversation going.

Scott at Boston.com comes up withe some great posts and I have posted another one below. Scott talks about a Redfin survey that finds only 46% of buyers surveyed think it is a good time for house hunting. This is apparent as well in all anecdotal information from the field specifically in downtown Boston. The issue remains lack of good available inventory and the impact that this will have in the “nascent real estate recovery. Jon

Posted by Scott Van Voorhis September 4, 2012 07:59 AM

Fewer than half the buyers out there – 46 percent – actually believe it is a good time to be house hunting, according to the online brokerage firm.

That’s a big shift from the first quarter, when hopes for deals and bargains was much higher among buyers as the spring sales season approached. Back then, 56 percent said it was good time to buy, Redfin notes.

However, probably the most dramatic change is in buyers’ expectations of where home prices are headed. The number of buyers who believe home prices are headed up has nearly doubled, to 61 percent from 32 percent in the first quarter.

So what’s made home buyers so glum?

Well bidding wars haven’t helped, with seven out of 10 buyers reporting they had encountered multiple bids on at least one offer, according to Redfin.

In fact, 31 percent of those surveyed said they would back off if confronted with another bidding war, up from 28 percent this spring.

Of course, at the root of the problem is a falling supply of homes for sale, a phenomenon that has endangered the nascent real estate recovery both here in Greater Boston and across the country.

Fewer choices have meant more bidding wars, rising prices and increasingly grumpy buyers. (The Redfin survey is based on the responses of 829 buyers during the week of Aug. 16-22.)

And the stumbling economy – and all those storm clouds over Europe’s rickety banking system – hasn’t helped cheer buyers up either.

The percentage of buyers worried about the economy rose to 27 percent from 20

percent in the first quarter.

We’ll just have to wait and see what the fall selling season brings, I guess.

484 Commercial Street, Provincetown $249K.

484 Commercial Street, Provincetown $249K. 293 Commercial St #3, Provincetown $249K

293 Commercial St #3, Provincetown $249K