August 9, 2013.

As the U.S. housing market gains, it’s taking the condominium market with it.

Home price growth in condos and co-ops is outpacing growth in single-family residences. This is a major shift for the housing market — condos were among the most distressed sectors of last decade’s housing market downturn.

Home sellers are getting higher prices for their condos.

Los Angeles Condos Jump 23%; Chicago Rises 12%

According to the most recent Case-Shiller Index, home values climbed 12.2 percent nationwide for the 12 months ending May 2013. This jump marks the biggest one-year increase in home valuation since the Case-Shiller Index launched 26 years ago.

Each of the Case-Shiller Index’s 20 tracked cities posted annual gains, led by the San Francisco Bay Area; Las Vegas, Nevada; and Phoenix, Arizona. Home valuations in the Las Vegas are up 23% since from 12 months ago, which claws back against the heavy losses sustained last decade.

The “last place” finisher in the May 2013 Case-Shiller Index? New York City.

As compared to one year ago, home values in the city’s five boroughs — Manhattan, Brooklyn, Queens, the Bronx, and Staten Island — rose just 3.3 percent, which is well below the U.S. national average.

However, the Case-Shiller headline figure tells just part of the story.

In New York City, the market is thick with condominiums and co-ops and it just so happens that the Case-Shiller Index ignores homes of these types. If we were to add back condos and co-ops to the Case-Shiller Index data, we’d actually see that New York City is performing quite well.

In New York, condo values are up nearly 10% since last year — well above the broader index’s reading of 3.3 percent.

The same is true in other Case-Shiller Index markets, too. Condos in the 4 other cities tracked by the Case-Shiller Condominium Index showed strong annual gains, and each outpaced its home city.

- Los Angeles, California : Condos +23.1% annually (versus +19.2% for single-family homes)

- San Francisco, California : Condos + 27.6% annually (versus +24.5% for single-family homes)

- Chicago, Illinois : Condos + 11.9% annually (versus +8.5% for single-family homes)

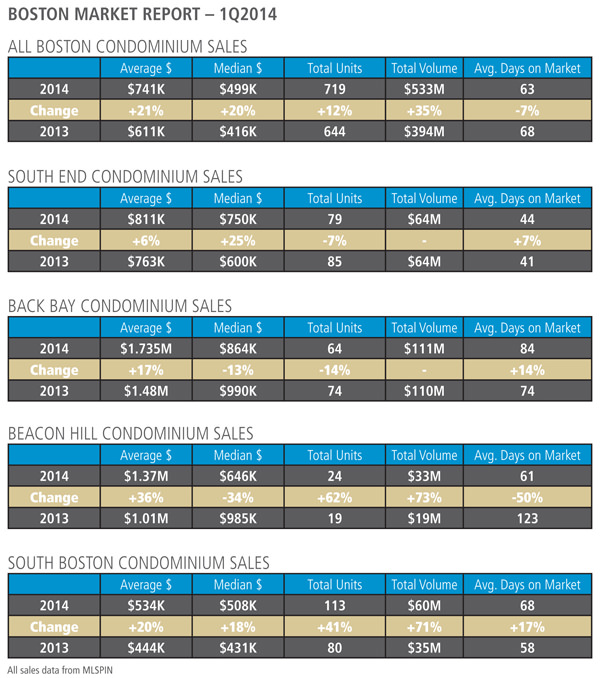

- Boston, Massachusetts : Condos +8.7% annually (versus +7.5% for single-family homes)

- New York City, New York : Condos + 9.8% annually (versus +3.3% for single-family homes)

With tight supply and limited construction, buyers of condos and co-ops should expect higher home prices through the end of 2013 and into early-2014, at least.

Mortgages For Condominiums

Getting a mortgage for a condo can sometimes be a challenge. Last decade, lenders were burned on condos for a variety of reasons and so they’ve bounced back on condo loans a bit more cautious and a bit more wise.

Today’s buyers of condos have fewer financing choices as compared to buyers of single-family detached homes.

As one example, buyers using conventional mortgage financing via Fannie Mae or Freddie Mac pay a premium for all loans with less than 25% equity. For this reason, buyers of condos and co-ops are encouraged to cap loans at 75% loan-to-value (LTV).

Condo loans above 75% LTV remain acceptable and approvable, however, the accompanying mortgage rate and/or closing costs will likely be higher.

VA loans for condos are available, too. VA loans allow 100% financing with no mortgage insurance required. Mortgage rates tend to be relatively low with a VA loan because all VA loans are guaranteed by the government.

In nearly all cases, though, buyers of condominiums will want to verify a building’s warrantability.

“Warrantability” is a mortgage term whether mortgages in a given condo building are eligible for purchase by Fannie Mae or Freddie Mac. Non-warrantable condos are sometimes denied for funding, but not always.

A building’s warrantability is based on a host of traits, some of which include :

- No person owns more than 10% of the building units

- No more than 50% of the building’s units are active rental units

- No more than 20% of the building is dedicated to commercial/retail space

To determine whether a building is warrantable or non-warrantable, mortgage lenders will often use a “condominium questionnaire”, which addresses the lendability of a building.

Non-warrantable condos can still be financed, it should be mentioned. Product availability, however, is limited and mortgage rates are sometimes higher.

The Case-Shiller Index reports rising values for today’s condos and co-ops. In many cases, condo prices have climbed more than for comparable single-family residences. Buyers of condos should expect rising prices.

About the Author

Dan Green (NMLS #227607) is an active loan officer with Waterstone Mortgage. You can also connect with Dan on Twitter and on Google+.

/cdn0.vox-cdn.com/uploads/chorus_image/image/54482731/Exterior___LJ.0.jpeg)

/cdn0.vox-cdn.com/uploads/chorus_asset/file/8418733/Rooftop_Terrace___LJ.JPG)

/cdn0.vox-cdn.com/uploads/chorus_asset/file/8418741/Living_Room___LJ.JPG)

/cdn0.vox-cdn.com/uploads/chorus_asset/file/8418745/Library_Lounge___LJ.JPG)