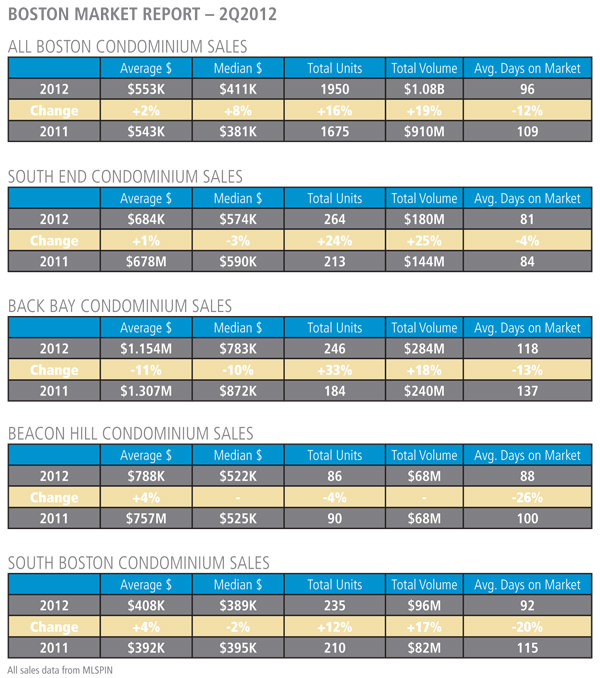

The Big Number is 16%. That’s the increase in condo sales in Boston as of June 30. Combined, all Boston neighborhoods saw a 16% increase in the number of condo sales year to date, a 2% increase in the average price of a condominium sold, and a 5% increase in the median sales price. Put together all this good news is more evidence that while not necessarily out of the woods, this real estate market is healthier than most. The one downside to this exceptional sales activity is that inventory levels of available condo’s for sale have fallen 38% to 1,177 properties for sale versus 1,903 at th is time last year.

Boston’s most expensive neighborhood the Back Bay, saw a 30% increase in sales while the average price of a condo sold dropped by 11% to $1.162M. The inventory level of properties for sale dropped 31% to 168 condos for sale vs 242 last year.

The South End saw a 24% increase in the number of condo sales to 264 properties and the average price of a condo sold increased 1% to $684K. The inventory of condos for sale decreased 45% from 208 to 114. Unless this condition corrects itself this will be a factor in market performance going forward.

South Boston, the darling of the my last market report moderated somewhat with a 4% increase in the average sales price to $408K and a 12% increase in sales to 235 properties sold through the second quarter. South Boston has the largest drop in inventory of all downtown n’hoods down 56% from 225 properties for sale last year to 99 available for sale today.

Every downtown neighborhood has it’s own story and most are positive excepting the inventory numbers. Total Boston numbers highlight the good news. Sales volume is up 19% to $1.080B… One Billion, 80 million dollars! Average days on market are down 12% and the inventory of properties for sale is down 38%. These numbers highlight incredible short term performance but portend serious issues going forward.